Tenpo's secured credit card was the first product of its kind in Chile. The mechanic existed regionally — Nubank had pioneered it in Brazil, and similar models ran in Mexico and Colombia — but no one had built it for the Chilean market.

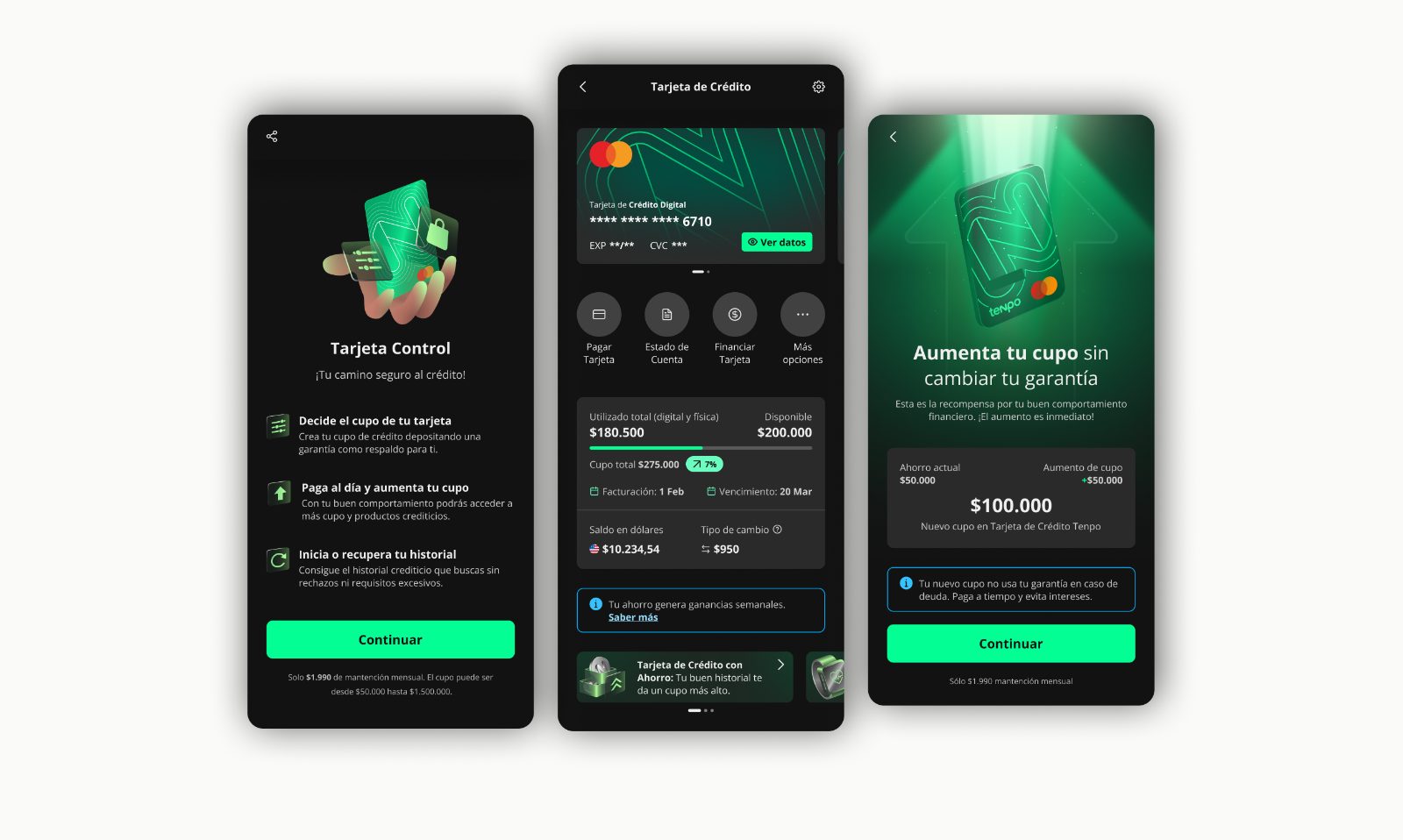

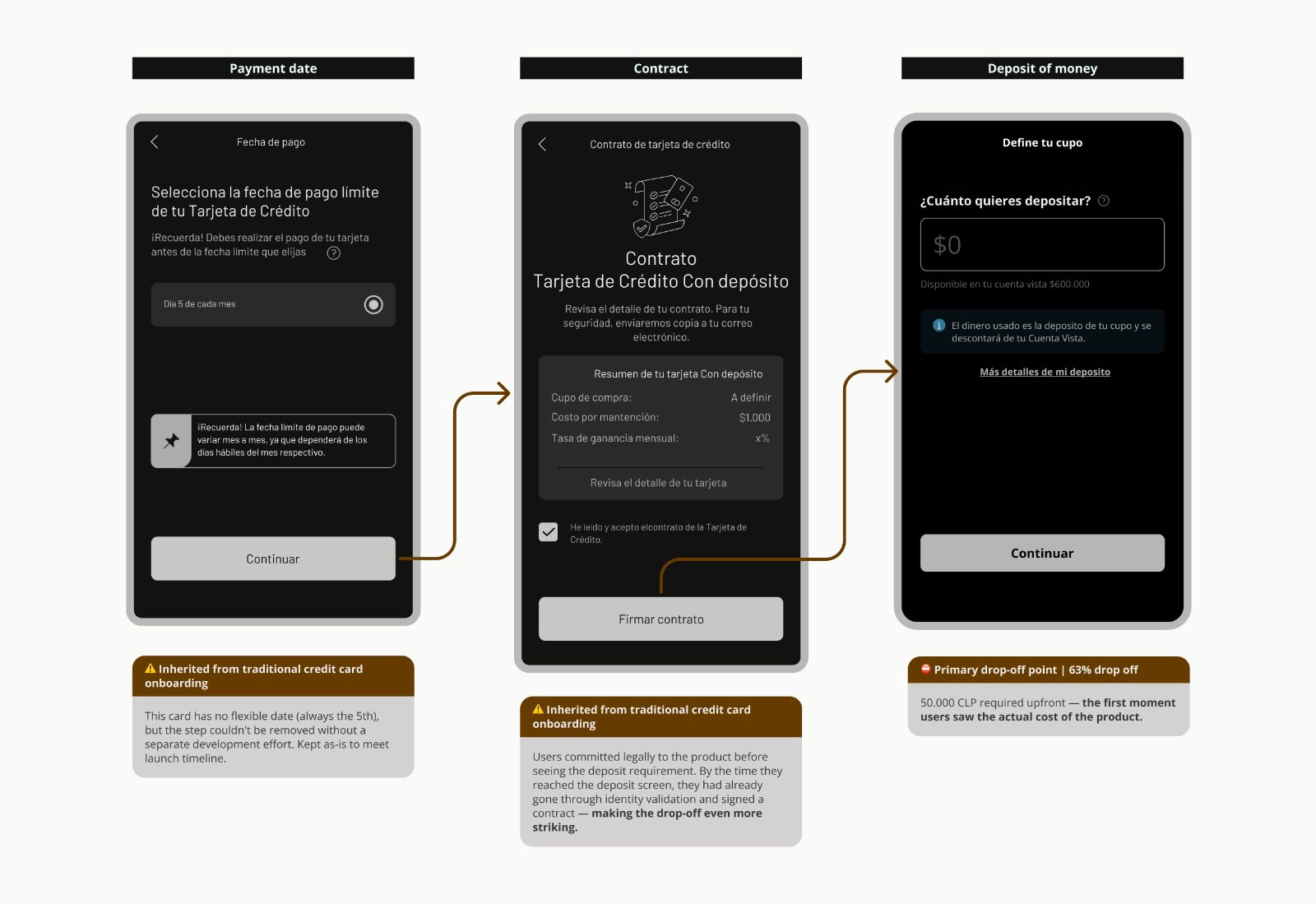

The product is straightforward: the user deposits 50.000 CLP, which becomes a fixed-term deposit and defines the card's credit limit. Unlike a prepaid card, the deposit isn't auto-debited — the user pays the monthly statement separately. The deposit stays put as long as payments are on time.

The target was two segments invisible to traditional banking: people without credit history (young adults, homemakers, first-time earners) and people with damaged credit scores. For Tenpo, this was financial inclusion plus a strategic on-ramp: bring underserved users in, build credit history, eventually graduate them to the unsecured card.

I joined in January 2024, at discovery. I'm still on it.

The cautious launch

Designing a financial product nobody in Chile had built before

Discovery started with two workshops. The first was internal — I facilitated a session with the PO, business stakeholders, and the credit team to surface assumptions, constraints, and what success looked like from each function. The second was with users from the target segment, to understand how they thought about credit, debt, financial visibility, and what kind of product would actually feel useful.

There was prior business research on the segment, which I built on rather than duplicated. The qualitative depth came from the workshops; the segmentation and market sizing came from the existing internal work.

Two early decisions shaped what we shipped.

Naming

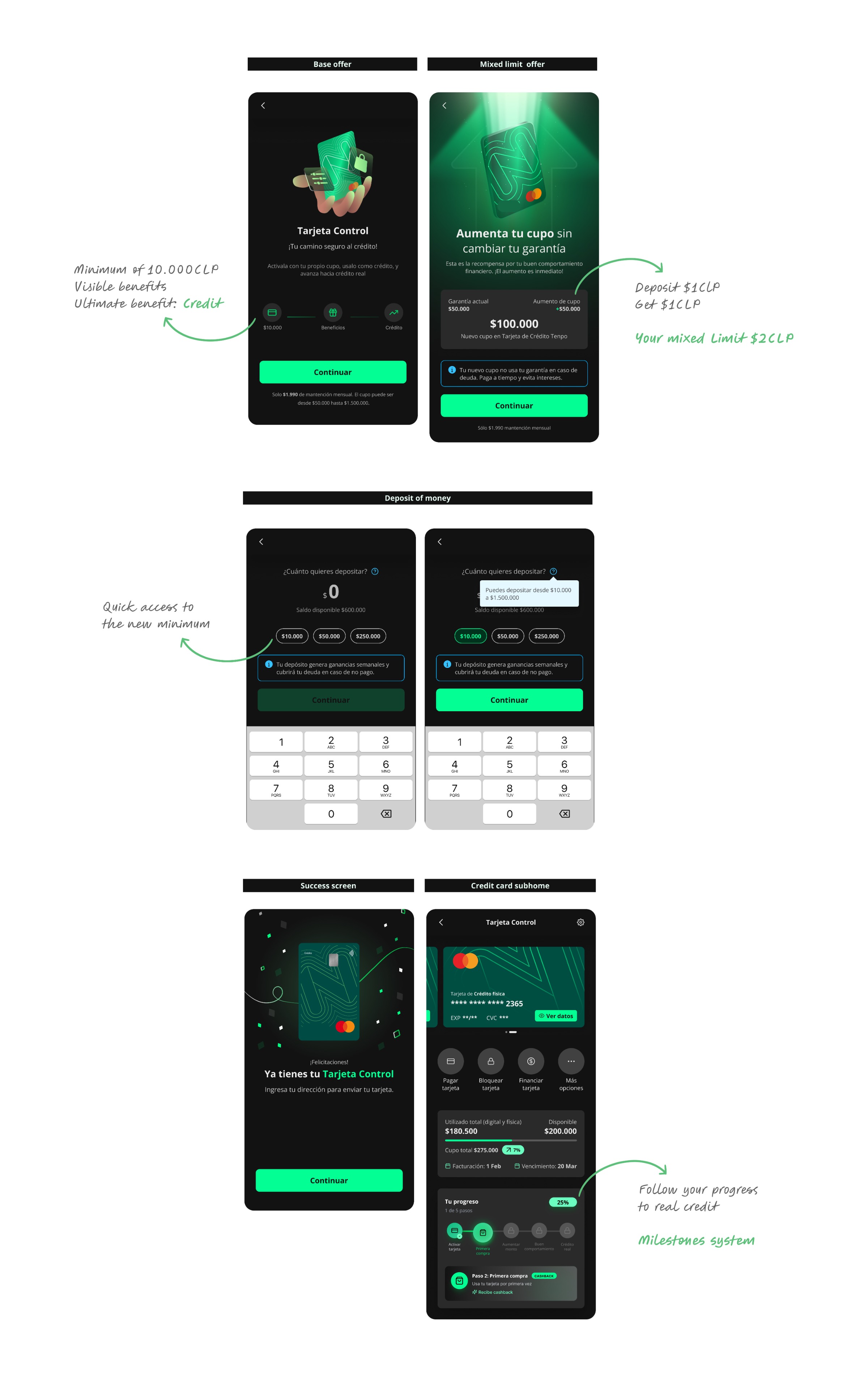

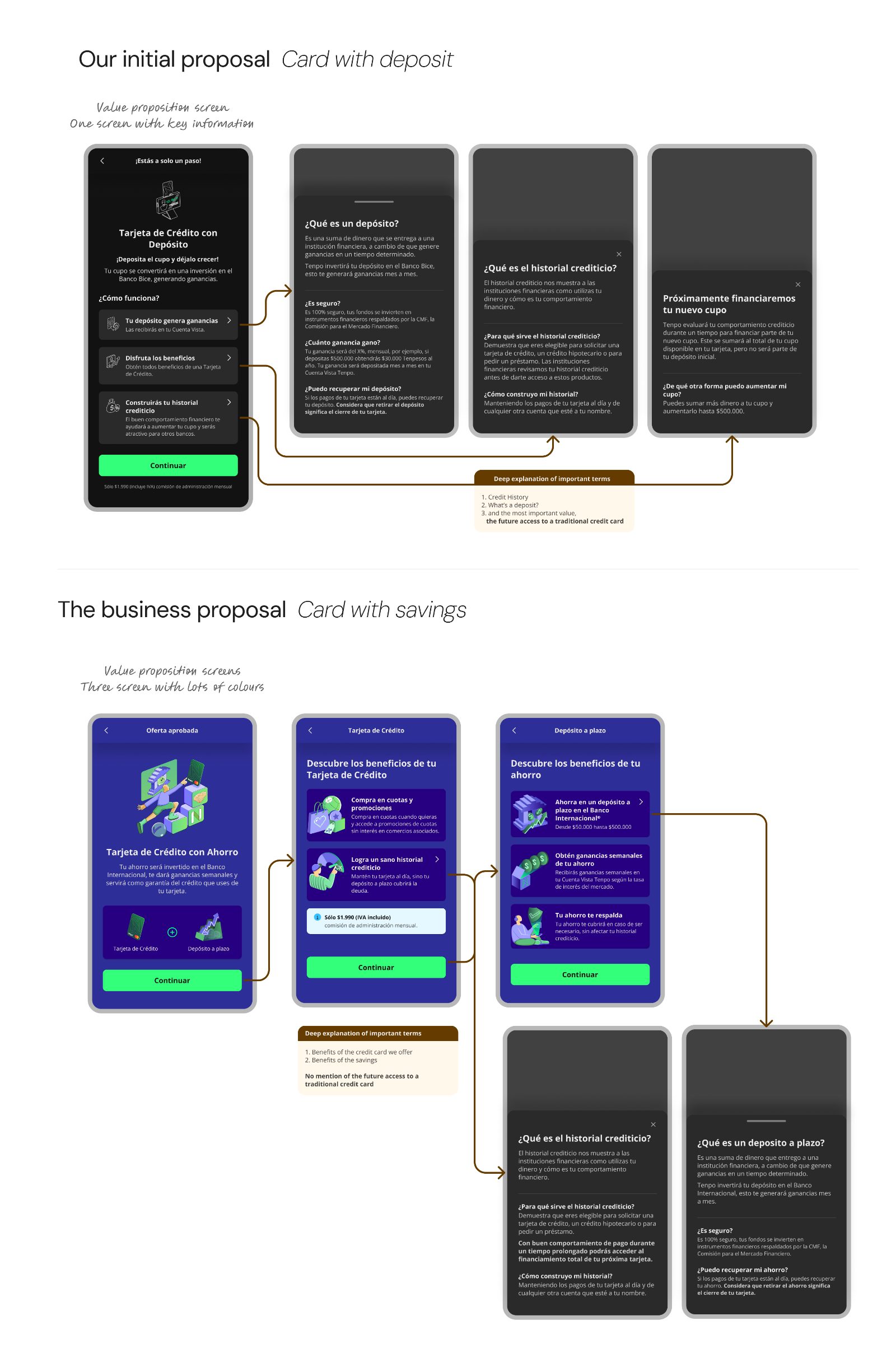

The product was originally going to be called tarjeta con garantía — "card with collateral." We tested the name with users and found it didn't communicate the product. The word garantía didn't connect to anything concrete. Tarjeta con depósito — "card with deposit" — landed better, because it described the actual action the user had to take. We changed the name before launch.

Reusing the existing onboarding

To meet the launch timeline, we built the new flow on top of the existing onboarding for Tenpo's traditional credit card. It was a deliberate trade-off: faster development, known constraints. We knew it would generate friction we'd have to work around later.

The product launched in July 2024 to a friends-and-family cohort. We tested the flow before launch, ironed out usability issues, and went live.

The result

The first hypothesis was almost mechanical: people wanted a credit card, but when they saw they had to deposit money to get one, they walked. The launch had also gone live at month-end, when liquidity is at its lowest in this segment. We assumed this was timing plus a self-selection effect, and that the numbers would correct.

They didn't.

The wrong hypothesis

Two teams, two diagnoses. Only one had data.

As the product underperformed, the diagnosis split.

The business team's reading was that users didn't understand the product. If we explained it better — clearer copy, sharper value proposition, more education in-app — conversion would follow. From the design and research side, my reading was different: comprehension was a real but secondary issue. The dominant barrier was liquidity.

While that disagreement played out, a separate problem appeared. The product started being communicated externally as tarjeta con ahorro — "card with savings." That introduced a third name into circulation alongside tarjeta con depósito (in-app) and tarjeta con garantía (legacy internal). We now had three names for one product, in a market that hadn't seen this product type before.

The deeper issue was misalignment of value. In-app communication framed the card around credit-building. External communication leaned on the deposit as a savings product — but the deposit's interest rate (~7% annually) was below market alternatives. We were selling two different products on two different surfaces, and neither was landing.

The research that resolved the disagreement

To move past internal debate, I led research designed to answer one question: what is actually stopping users at the deposit step?

— 01 · Interviews

Users in the target segment who dropped or never started.

+20 interviews · Google Meet and phone calls— 02 · Surveys

Extending qualitative findings to a larger sample.

Pattern validation— 03 · Guerrilla testing

In-context sessions executed by the Chile design team.

Protocols designed remotely from BA— 04 · Behavioral analysis

UXCam session reviews and funnel analysis on the deposit step.

Quantitative triangulationWhat we found

Comprehension was real but not dominant

About 60% of users understood the product correctly. About 40% didn't fully understand, and some confused it with a prepaid card. So there was a comprehension problem — but it wasn't the bottleneck.

Liquidity was the dominant barrier

The vast majority of interviewed users simply didn't have 50.000 CLP available to leave immobilized. Not "didn't want to" — didn't have.

There was a viable threshold

When asked what amount they could realistically commit, users converged around 10.000 CLP. Many also liked the idea of starting low and increasing the limit progressively as they gained confidence in the product.

This reframed the conversation. The product wasn't failing because users misunderstood it. It was failing because we were asking too much from a segment defined by having too little.